How tokenized deposits differ from deposit tokens and asset tokenization, the core principles behind their design and the emerging architecture shaping next-gen banking.

1) Introduction

2) What exactly are “tokenized deposits” - and what properties do they have?

2.1 Tokenized deposits are regulated separately from crypto

2.2 Tokenized deposits follow the same backing and protection rules as bank deposits

2.3 Tokenized deposits must be the same entity as bank deposits

2.4 Programmability and automation

3) Tokenized deposits or deposit tokens?

3.1 Similarities between tokenized deposits and deposit tokens

3.2 Differences between tokenized deposits and deposit tokens

3.3 How they compare to other types of tokens

4) Use cases, risks, and potential challenges

5) Conclusion

1. Introduction

What are tokenized deposits? The term sounds close to tokenization and LP tokens. And some sources even confuse “tokenized deposits” with asset tokenization, which distorts how people understand and interpret them. Yet tokenized deposits could be a breakthrough for the entire global banking system. It’s simultaneously a simple concept on the surface - and deeply complex underneath.

They’re described as digital representations of deposits with programmability advantages, 24/7 transfers, AML/KYC compatibility, and direct settlement capabilities between banks and various counterparties. Another interpretation: “the process of recording rights to financial or real assets that exist on a traditional ledger onto a programmable platform” - which also captures the principle of deposit/account programmability.

BRRR DAO is a team of experienced Web3 enthusiasts with diverse expertise, committed to actively participating in the evolution of the blockchain industry.

This makes it more like an account model rather than creating derivatives or tokens in the traditional sense. Unlike bank accounts - controlled by numerous separate programs with staff involvement - crypto accounts on smart contract platforms can be configured in various ways. With Account Abstraction (AA), for instance, they can even gain some autonomy depending on their algorithms. Where banking infrastructure uses different programs with different access rights running on various instances (often from different vendors) to manage money flows, blockchain consolidates everything within smart contract parameters and conditions that also govern account behavior.

This isn’t possible on all chains. On Ethereum and most EVM chains, it works thanks to ERC-4337 and EIP-3074/7560. But there are still many gray areas around tokenized deposits since this remains in the research and theorization stage. These include connections to banking systems, compliance, and developing networks that need to be simultaneously permissioned and permissionless.

That’s why this research examines different perspectives and models for representing tokenized deposits. As of late 2025, there are many opinions and theories shaping this technology - so quotes are an integral part of this analysis.

2. What exactly are “tokenized deposits” - and what properties do they have?

As mentioned above, “tokenized deposits” have two main definitions:

- Digital representations of deposits with programmability advantages, 24/7 transfers, AML/KYC compatibility, and direct settlement capabilities between banks and various counterparties

- The process of recording rights to financial or real assets that exist on a traditional ledger onto a programmable platform

This sounds similar to familiar crypto systems and DeFi. But both formulations pursue one very important idea: tokenized deposits ≠ crypto and DeFi. In fact, they relate to web3 about as much as current bank accounts relate to trading on Unichain.

You might ask: Revolut users can hold crypto in their accounts - isn’t that tokenized deposits? No. Revolut uses custodial services to store users’ crypto, but users don’t even see a digital representation of their assets - rather, they see a virtual display of crypto asset balances. Tokenized deposits are something entirely different.

We’ve identified several core principles based on numerous studies and materials:

- Not crypto according to regulatory relationships - these are bank deposits

- Unlike crypto assets, tokenized deposits are backed by banks’ real money and government bonds - again characteristic of bank deposits

- The bank account and its DLT representation are a single entity

- Unlike tokenized assets and CBDCs, tokenized deposits have broad programmability, increasing their functionality

2.1 Tokenized deposits are regulated separately from crypto

In the Eurozone, for example, tokenized deposits don’t fall under crypto regulation with MiCAR provisions aimed at regulating crypto. This is confirmed by many sources. A Freshfields article notes that tokenized deposits aren’t necessarily analogous to deposits like an account in a wallet - they can also be tokens:

“The token may exist instead of or in addition to a central bank ledger (i.e. an off-chain bank account). The claim against the credit institution may be ‘account-based’ i.e. linked to the account holder’s identity, or ‘token-based’ i.e. solely linked to the token holder (like a bearer instrument).”

And furthermore, it is confirmed:

“MiCAR relies on the deposit definition established by the Deposit Guarantee Scheme Directive. Tokenized deposits that qualify under the exemption are potentially eligible for deposit protection.”

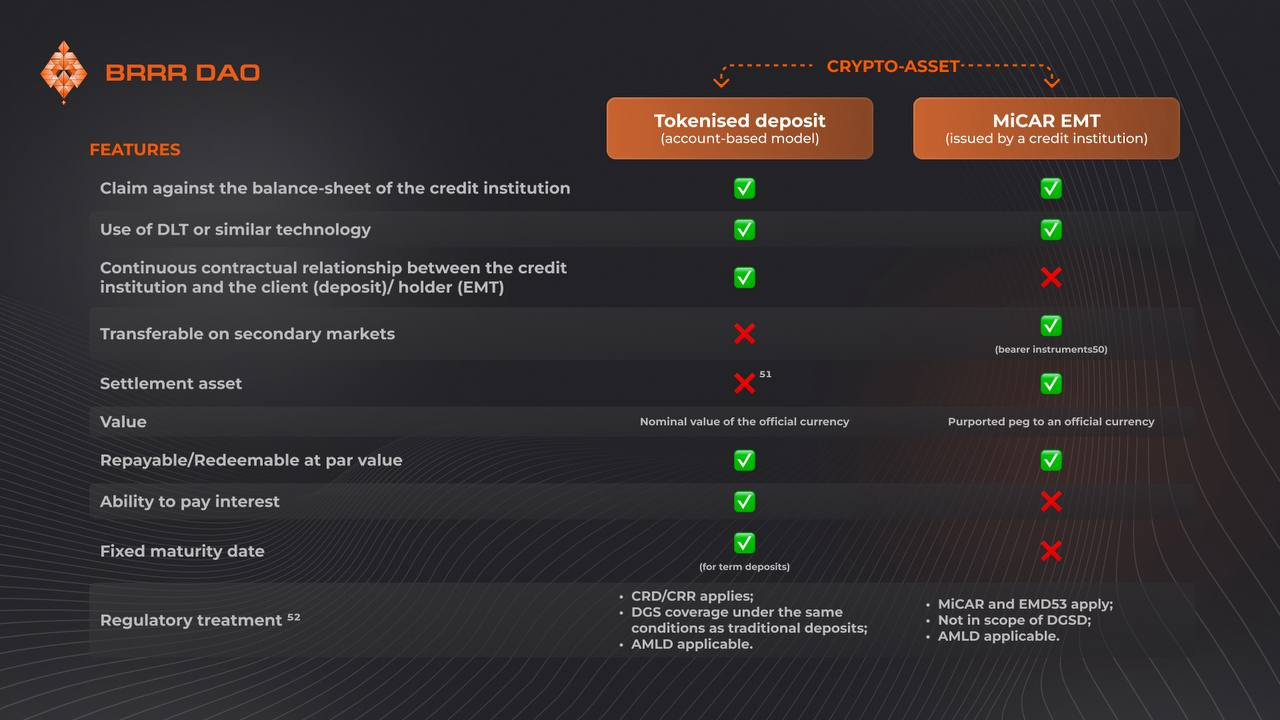

The European Banking Authority (EBA) research also provides a comparative distinction between tokenized deposits and MiCAR EMT (”E-Money Token” - a type of crypto asset designed to maintain stable value by pegging to an official fiat currency):

This has some collisions in other jurisdictions (covered in a separate section), but the general understanding is clear: crypto wallets with stablecoins are separate, while crypto-technology-based components for banking infrastructure are separate. There’s still debate about whether tokenized deposits can function as tokens similar to LP tokens - but we’ll address that later.

The main point: at the legislative and regulatory level, everything concerning bank deposits is strictly TradFi, and this cannot be natively connected to web3.

2.2 Tokenized deposits follow the same backing and protection rules as bank deposits

One of the most important properties of tokenized deposits compared to stablecoin wallet accounts is that they’re backed by banks’ real money and government bonds - just like regular bank deposits.

Back in 2023, the BIS Bulletin “Stablecoins versus Tokenised Deposits: Implications for the Singleness of Money” analyzed structural differences between stablecoins and tokenized deposits:

“The model of tokenised deposits envisages participants to be customers of regulated financial institutions (such as banks), and transfers are recorded at the individual bank level and settled automatically using tokenised central bank money (ie CBDC).”

This indicates that tokenized deposits reflect traditional banking obligations backed by customer relationships and bank assets, while stablecoins rely on asset-backed reserves that can lead to value deviations.

Key backing discussion points:

- Tokenized deposits are backed by the issuing bank’s obligations to customers, with central bank money settlements guaranteeing nominal value. They’re integrated into existing regulatory frameworks and provide guarantees similar to commercial bank deposits.

- Stablecoins are asset-backed with value tied to issuer reliability for redemption, but specific reserves like government bonds aren’t specified - the focus is on potential friction related to credit risk.

Michael S. Barr confirms this in “Exploring the Possibilities and Risks of New Payment Technologies”, criticizing stablecoins for relying on potentially volatile reserves unlike tokenized deposits:

“Stablecoins are typically backed by a range of non-cash reserve assets, such as uninsured deposits or other volatile items... Tokenized deposits, by contrast, are implied to align with bank-issued assets, benefiting from robust regulatory oversight.”

William Chen and Gregory Phelan in “Digital currency and banking-sector stability” also confirm that the key difference is stability:

“In contrast to stablecoins, which are backed by debt, tokenized deposits backed by traditional bank assets improve welfare without harming financial stability.”

This thesis appears in numerous sources, including JP Morgan and McKinsey research on tokenized deposits (or Deposit Tokens). And it’s inseparably linked to the previous point - tokenized deposits aren’t just regulated like bank accounts, they inherit their fundamental principles.

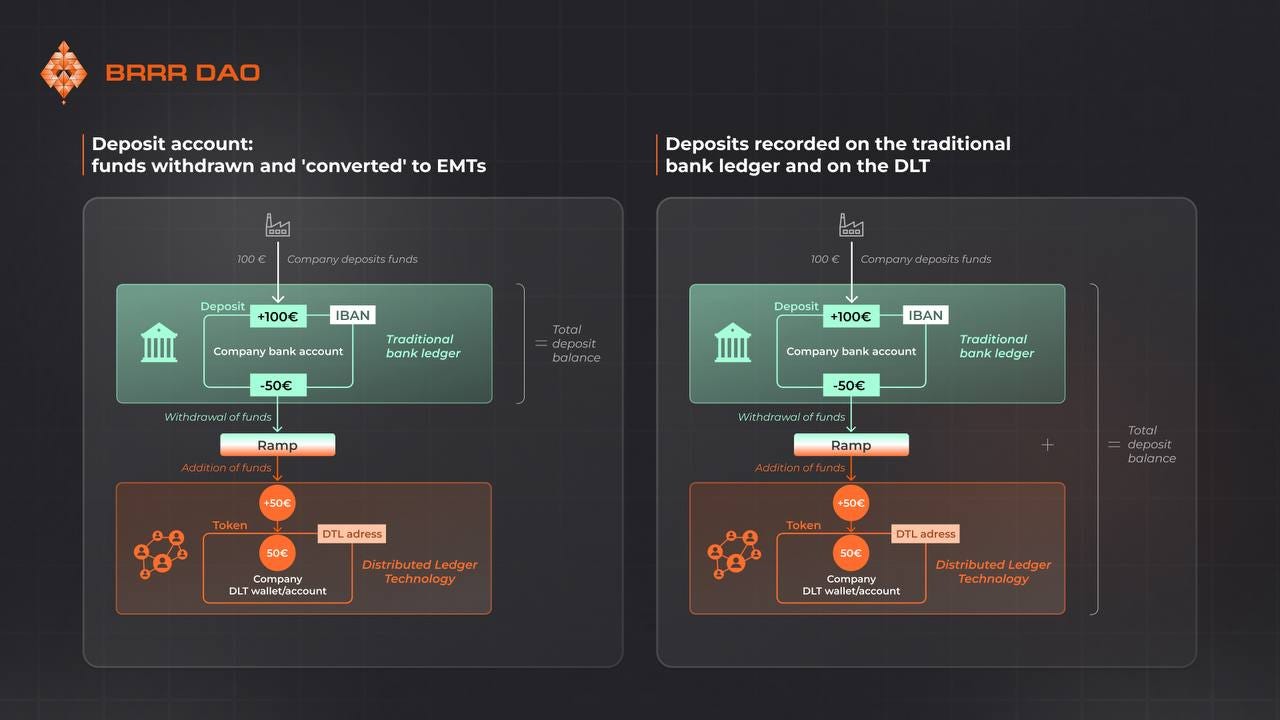

2.3 Tokenized deposits must be the same entity as bank deposits

The next critically important aspect: with simple tokenization, the bank account and DLT (blockchain) account are separate. With tokenized deposits, they’re unified into a single account (as confirmed by EBA research). They can also include deposit insurance - impossible with stablecoins, and requiring traditional banking infrastructure participation for CBDCs.

CBDCs, like stablecoins, are representations (tokenizations) of government currency but not accounts - so they exist in parallel.

The visualization of tokenized deposits from the HKMA also shows the combination of bank deposits and DLT deposits. To some extent, this is similar to a deposit account, since after a transaction in DLT, banks exchange cross-border transfer settlements with each other using SWIFT and RTGS to reconcile currency and cash balances for transactions. On the other hand, maintaining the traditional banking infrastructure may be necessary both to enable working with structures that do not have DLT and to ensure reliability.

2.4 Programmability and automation

The difference from traditional banking infrastructure is that staff involvement isn’t required for these operations - automation can be implemented through smart contracts with various lists, permissions, and administration policies.

This is the key distinction between tokenized deposits and Stablecoins/CBDCs, which are essentially tokens representing monetary assets in digital form and can exist parallel to existing banking infrastructure.

Theses about the programmability of tokenized deposits are confirmed by banks that are directly involved in research in this area:

J.P. Morgan Report: “Deposit Tokens” (2025):

“The programmable nature of deposit tokens enables innovative solutions to support existing deposit-taking activities, such as the conditional transfer of funds based on conditions at a smart-contract level, as well as related banking services, such as conditional intra-day lending decisions or disbursement of interest payments.”

KPMG Report: “Deposit Tokens: Bridging Traditional Banking and the Digital Economy” (2025):

“Like other digital assets, tokenized deposits can be programmed with smart contracts, enabling automated, conditional transactions. This feature opens a world of possibilities for innovative financial products and services and for achieving ultra-efficient payments.”

Academic research also supports this, such as “Tokenized Deposits” by Damiano Topputi:

“With the utilization of smart contracts, tokenized deposits can be managed in a transparent and independent way, reducing risks of human error and operational costs. A tokenized deposit, for example, may be programmed to transfer funds electronically to a recipient without requiring a specific condition to be met (for example, payment of a benefit or service).”

Spydra provides one of the most practical examples with real use cases in “Deposit Tokenization: How Tokenized Deposits Are Reshaping Banking”:

“Because deposit tokens reside on a programmable ledger, banks or users can embed logic via smart contracts: Conditional payments (e.g. release funds when shipment arrives), Automated interest accrual or payouts, Escrow services, Automated collateralization. This opens up new service models where deposits become not just static balances, but active financial tools.”

HKMA’s March 2025 research “Distributed Ledger Technology in the Financial Sector” examines tokenized deposits and clearly highlights 24/7 operation without traditional clearing system limitations:

These same theses appear in various forms across many other researches and publications - Bank Policy Institute (BPI) Report: “Distributed Ledger Technology: A Case Study of the Regulatory Approach to Banks’ Use of New Technology” (February 2024), Swiss Banking Association Report: “The Deposit Token”, Visa Report: “e-HKD Pilot Programme: Tokenised Deposits” (2025) and others.

Smart contract automation on-chain substantially differentiates tokenized deposits from regular banking systemsoperating through various software with staff involvement - and from stablecoins and CBDCs, which are merely assets.

Here’s what the current multi-currency transfer process between banks in different countries looks like according to MAS (Monetary Authority of Singapore) visualization in “Use of Tokenised Bank Liabilities for Transaction Banking”:

With DLT and smart contracts, this becomes a much simpler process (assuming transactions will likely be duplicated in traditional systems for reliability):

3. Tokenized deposits or deposit tokens?

In the evolving digital finance space, terms like “tokenized deposits” and “deposit tokens” are often used interchangeably - but they require closer examination to understand their nuances, similarities, and differences.

“Deposit Tokens” specifically appears in JP Morgan’s joint research with Oliver Wyman (”Deposit Tokens”) and in KPMG’s article “Deposit Tokens: Bridging traditional banking and the digital economy”. So the question arises: are these the same thing, or actually different?

After studying various sources, we concluded this has two sides: terminology confusion in most sources, yet also distinction between these terms. At their core, both concepts refer to representing traditional bank deposits as digital tokens on blockchain. This enables enhanced programmability, faster settlements, and seamless integration with decentralized finance (DeFi) ecosystems.

However, subtle differences in terminology and implementation can arise depending on context - such as regulatory frameworks or issuing institutions. Below we examine these aspects, using examples like JP Morgan’s deposit token research to illustrate key points.

3.1 Similarities between tokenized deposits and deposit tokens

Tokenized deposits and deposit tokens share fundamental characteristics bridging traditional banking with blockchain technology. Both aim to digitize fiat currency held in bank accounts, making it more efficient for transactions in the digital world.

- Blockchain representation: Both are digital tokens representing claims on underlying bank deposits. They use distributed ledger technology (DLT) to enable direct peer-to-peer transfers without intermediaries, reducing settlement times from days to seconds.

- 1:1 backing and stability: Unlike volatile cryptocurrencies, these tokens are typically backed 1:1 by fiat currency in regulated bank accounts. This provides price stability similar to stablecoins but with added security from direct linkage to bank deposits.

- Programmability and use cases: They support smart contract functionality, enabling automated payments, escrow services, or conditional transfers. For international payments or securities settlement, both can enable instant 24/7 operations.

- Regulatory compliance: Since they’re issued by licensed financial institutions, they comply with banking regulations including anti-money laundering (AML) and know-your-customer (KYC) requirements. This makes them more institutionally friendly than unregulated crypto tokens.

Essentially, similarities stem from their shared goal: modernizing deposits through tokenization, enhancing liquidity and accessibility while maintaining trust associated with traditional banking.

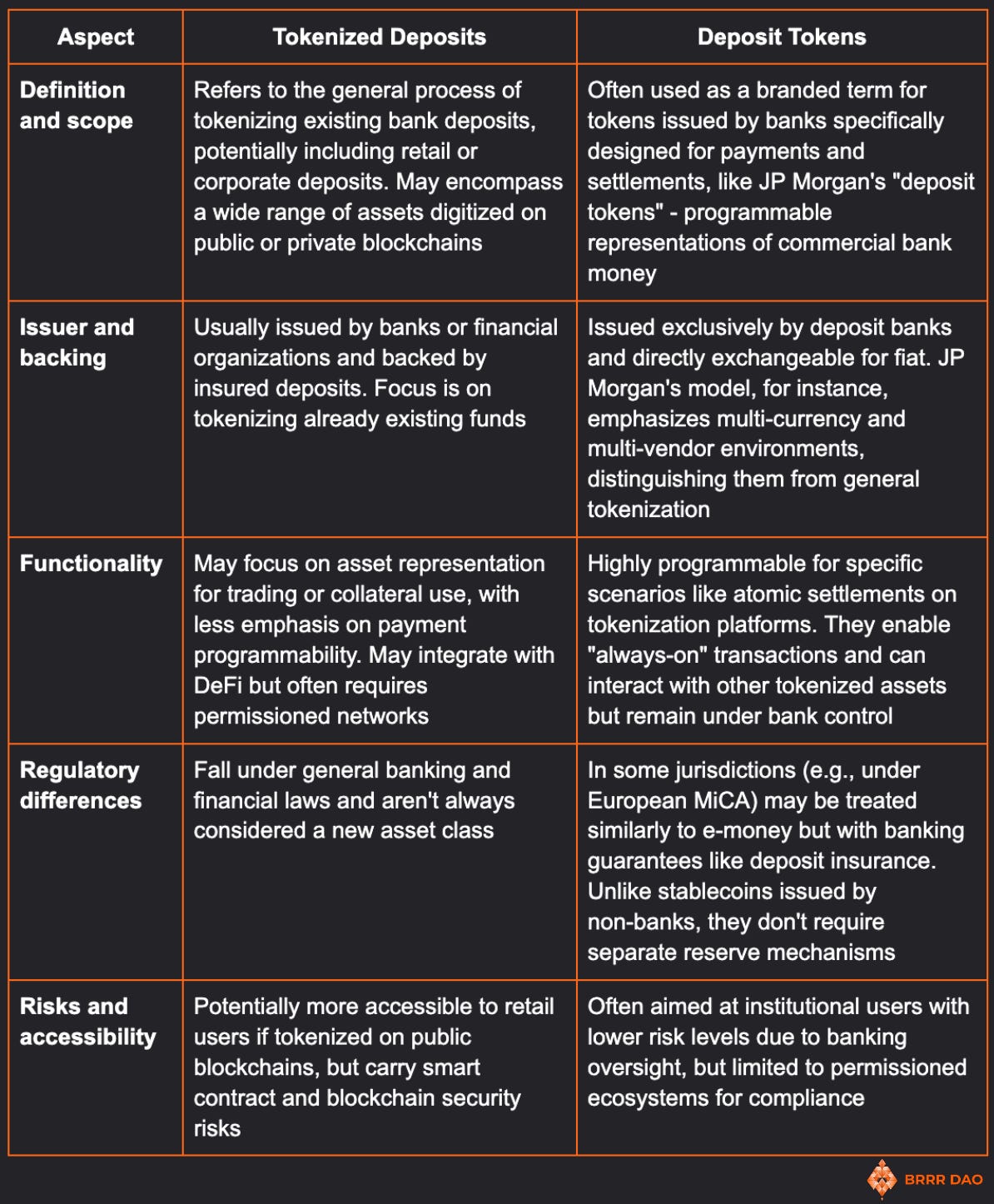

3.2 Differences between tokenized deposits and deposit tokens

While the terms are considered synonymous in many discussions, some sources distinguish them based on scope, issuance, or functionality.

“Tokenized deposits” often broadly describes the process of converting any bank deposit into a blockchain token, while “deposit tokens” may refer to specific products designed for programmable payments - like those offered by JP Morgan.

The Oliver Wyman article “How Deposit Tokens Are Changing The Digital Money Ecosystem” also highlights differences between “tokenized deposits” and “deposit tokens”. Deutsche Bank likewise distinguishes between them. Tom Zach, CIO of SWIFT, also clearly separates tokenized deposits and deposit tokens in his Twitter thread, emphasizing the difference exists.

These differences highlight that “deposit tokens” can be viewed as a refined subset of tokenized deposits optimized for corporate applications. In JP Morgan’s framework, deposit tokens are positioned as tools allowing banks to maintain control over money while using blockchain - unlike tokenized deposits, which may be more experimental or DeFi-oriented.

3.3 How they compare to other types of tokens

To fully understand these concepts, it’s useful to compare them with broader “tokens” in the crypto space - utility tokens, security tokens, or stablecoins.

- Vs. cryptocurrencies (e.g., Bitcoin or Ethereum): Tokenized deposits/deposit tokens are stable and asset-backed, while cryptocurrencies are speculative, decentralized, and not redeemable for fiat. The former focus on payment utility; the latter on store of value or governance.

- Vs. stablecoins (e.g., USDC or Tether): Both offer stability, but stablecoins are often issued by non-banking entities and their reserves may include government bonds or commercial paper. Tokenized deposits, being bank-issued, benefit from deposit insurance (e.g., FDIC in the US) and direct central bank access, reducing counterparty credit risk.

- Vs. e-money tokens (CBDC): In regions like the EU, e-money is issued by e-money institutions and functions like prepaid cards. Deposit tokens differ by originating from banks, enabling interest accrual and deeper integration with traditional finance.

Ultimately, tokenized deposits and deposit tokens represent convergence between banking and blockchain, blurring lines between fiat and digital assets. Their adoption could transform financial infrastructure, but success depends on regulatory clarity and interoperability. As this space evolves, the distinction between these terms may fade, giving way to a unified category of programmable bank money.

4. Use cases, risks, and potential challenges

Based on the principles and definitions above, it’s clear that tokenized deposits have substantial differences from CBDCs and crypto. To understand subsequent processes in later parts, we need to outline their use cases, risks, and potential challenges.

Use cases for tokenized deposits:

- Transferring balances from traditional accounts to on-chain tokens within a single bank

- Interbank settlements with token transfers between banks, including RTGS (real-time gross settlement) integration

- Multi-functional scenarios including multi-currency settlements and smart contract use for automating payments and delivery settlements

- Real-time and atomic settlement via tokenized deposits and cash/assets on-chain for interbank payments (from “Tokenization and Financial Market Inefficiencies”)

- Unlike CBDCs (closest in regulatory context), tokenized deposits enable automated interest accrual - stemming from their programmability

Benefits vs. regular accounts (programmable deposits eliminating complex internal banking operations and bureaucracy):

- Programmability: ability to automate payments and transaction execution conditions

- Instant and atomic settlements: money and assets can exchange simultaneously without counterparty risks

- In this research, deposit tokens are viewed as competition to CBDCs and digital currencies

- Staff independence: smart contract-based systems work without ties to banking holidays or cut-off times (though this is also a downside - some movements may still require manual confirmations/verification for suspicious actions, which negates this thesis)

- Increased efficiency: programmability, automation, atomicity of operations

- Improved AML/CFT control thanks to immutability, cryptographic protection, and full data availability

Risks:

- Neobanks might implement this first - but they’re not a threat to large banks and use their infrastructure; lobbies will unlikely welcome processes going “outside,” so such technologies should probably be permissioned

- Overly complex banking infrastructure provides many jobs and software development opportunities - which in turn creates additional jobs and financial flows

- Risk of slowing open public initiatives from regulator and bank lobbies

- Previous point leads to conclusion: when such technologies are implemented and leave R&D stage, they should be controlled by banking structures and developed on their side for full control

- Confirming above theses, deposit token issuance is assumed to be by financial institutions, not private firms, reducing concentration risk and making them more decentralized from an issuer perspective. But this actually creates infrastructure and regulation centralization risks - especially critical given the current world order with sanctions and blockages

- Specifically regarding JPMD (source): It has limited value for global settlements since it only works between clients of one bank and isn’t a generally accepted payment method. Interoperability is questionable. Lack of full interoperability will allow large banks to maintain their spheres of influence.

Key vulnerabilities, which are also mentioned in the FSB research, that may manifest when scaling tokenization (as they specifically call tokenized deposits):

- Liquidity and maturity mismatch: risk when quickly converting tokens to cash or traditional assets

- Leverage: tokenized assets may be used with increased leverage

- Asset price and quality: possible divergence between tokens and underlying assets, plus asset quality risks

- Interconnectedness: technologies, especially smart contracts and composability, create complex dependencies between market participants

- Operational risks: technical failures, infrastructure issues, third-party providers: custody, oracles, bridges between DLT platforms

Challenges:

- Consumer protection: need for technological and financial literacy, risks of digital exclusion and confusion with EMTs and other crypto assets

- Regulatory classification: difficulty distinguishing tokenized deposits from EMTs

- Operational risks: DLT attacks (e.g., 51% on public blockchains), technical failures, infrastructure provider dependencies

- Liquidity management: programmability may exacerbate deposit fluidity and increase sudden outflow risks

- AML/CFT legal aspects: need to clearly define when a transaction is a “funds” transfer vs. “crypto-assets” transfer, especially with updated regulation (FTR recast)

When banks have international divisions, compliance with different regulatory norms becomes problematic - potentially causing technical dispersion and fragmentation. Different standards exist with different deposit requirements - FDIA and BSA in the US; CRR, CRD, and PSD2 in the EU; CBIRC in China; and many others.

Permissionless chains: On one hand, deploying on them ensures decentralization and transparency. On the other - there’s no controlled access needed for compliance with interbank netting or settlement finality, which may violate standards like Bank for International Settlements (BIS).

Thus, tokenized deposits have both advantages over traditional accounts (with substantial differences from crypto accounts) and certain risks and challenges. They may have opponents due to eliminating human factors from infrastructure and existing technical stacks capable of cross-border and interbank transfers. With tokenized deposit technology, regulators and banks will face not only technological fragmentation but also regional fragmentation.

Among possible fragmentation paths are requirements from FDIA, BSA, CRR, CRD, PSD2, CBIRC, and many other local regulatory acts in different jurisdictions. For example, reserve requirements relative to deposits: US is 0% since 2020 for flexibility; EU is ~1% set by ECB; China applies high rates (7–8%) for money supply control; India is ~4%. Beyond insurance coverage differences, there’s another important aspect - fund availability and clearing. In the US, Regulation CC requires access to some checks next day, using ACH/Fedwire for settlements. In the EU, PSD2 enables instant payments via SEPA with API integrations for open banking. UK uses Faster Payments Service; China uses high-performance systems like IBPS.

This affects backend infrastructure - for example, real-time gross settlement systems (RTGS) in the EU (TARGET2) vs. net settlements in some US cases - leading to differences in transaction speed, fraud checks, and API requirements. All this must be considered when building automated systems and permissions. Beyond this, there are technical aspects regarding cross-chain interaction between different DLTs with different transaction finalization times.

We’ve established that tokenized deposits don’t fall under crypto regulation legislation like the US GENIUS Act and EU’s MiCAR. But there are no clear definitions or guidelines for cases where tokenized deposits are deployed on permissionless chains - theoretically, they could fall under MiCAR in this case. Such borderline regulations include the Payment Services Act (PSA) under MAS, which regulates digital payment tokens and systems, is more innovation-oriented than MiCAR but simultaneously stricter regarding cross-border operations than GENIUS.

5. Conclusion

Tokenized deposits are quite a multifaceted topic, despite the seemingly simple definition. Even setting aside the confusion between “tokenized deposits” and “deposit tokens” (which can be distinguished) and basing functionality on bank deposits - this remains a highly uncertain zone.

On one hand, there’s already established banking infrastructure, and transitioning to new systems will take considerable time. This is amplified by the fact that when equated to bank deposits, tokenized deposits don’t gain expanded interaction with DeFi and public web3 infrastructure.

This uncertainty is further amplified by various implementation variations from different TradFi players. For example, no direct contact with crypto and web3 implies launching in isolated instances - say, based on Hyperledger. But there are also pilot project implementations on public blockchains like Ethereum and Base, which also blurs the regulatory base.

One thing can be clearly determined right now: tokenized deposits will likely only follow standard bank deposit regulation rules if they’re on permissioned DLT. In this case, technical base fragmentation arises, requiring connections between different DLTs with different settings and implementations. Moreover, this can’t work on existing public cross-chain protocols since infrastructure control and strict regulatory compliance would be violated.

This part of the series covered the theoretical portion with a general approach. In the next part, we’ll examine practical tokenized deposit implementations from JP Morgan, BNY Mellon, Swiss Banking Association, and other players - with differences in approaches across various frameworks and jurisdictions for deeper immersion in the topic.

BRRR DAO

Is a team of experienced Web3 enthusiasts with diverse expertise, committed to actively participating in the evolution of the blockchain industry. Deep in our vision: Introducing ₿RRR DAO: Frontier Founders.